How Net Rate (Raw Rate), Construction Estimating, and FALIB® Reporting Impact Workers’ Comp and Profitability

The most important factor when negotiating a better workers’ compensation rate is knowing your net rate (raw rate). This is your true multiplier on payroll, and without it, accurate estimating, pricing, and financial forecasting become extremely difficult.

For companies using structured systems like FALIB® and BreakEven+™, the net rate is a required input for construction estimating, break-even analysis, and business forecasting.

• Net rate (raw rate) is your true labor multiplier

• Scheduled credit impacts your real discount more than most realize

• Incorrect rates lead to bad estimating and forecasting

• FALIB® + BreakEven+™ align estimating with real financial outcomes

What Is the Net Rate (Raw Rate)?

The net rate (also known as the raw rate) is the final multiplier applied to payroll that determines your actual workers’ comp cost. Insurance carriers typically do not provide this number directly — which creates a major gap in financial visibility.

This is exactly why structured reporting systems like FALIB® exist — to bring clarity to these hidden cost layers.

Why Net Rate Matters in Estimating and FALIB®

When building estimates, your pricing must reflect your true labor burden. The net rate is a critical component of that burden.

- Ensures labor cost is fully captured

- Allows BreakEven+™ to calculate accurate break-even points

- Gives analysts real profitability instead of assumed margins

How to Get a Better Net Rate

Improving your net rate comes down to two key factors:

- Experience Mod (EMR)

- Negotiated (Scheduled) Credit

While your experience mod impacts risk, the largest reduction in premium typically comes from your negotiated credit.

What matters most is not just the dollar amount — but the percentage, which directly affects your net rate.

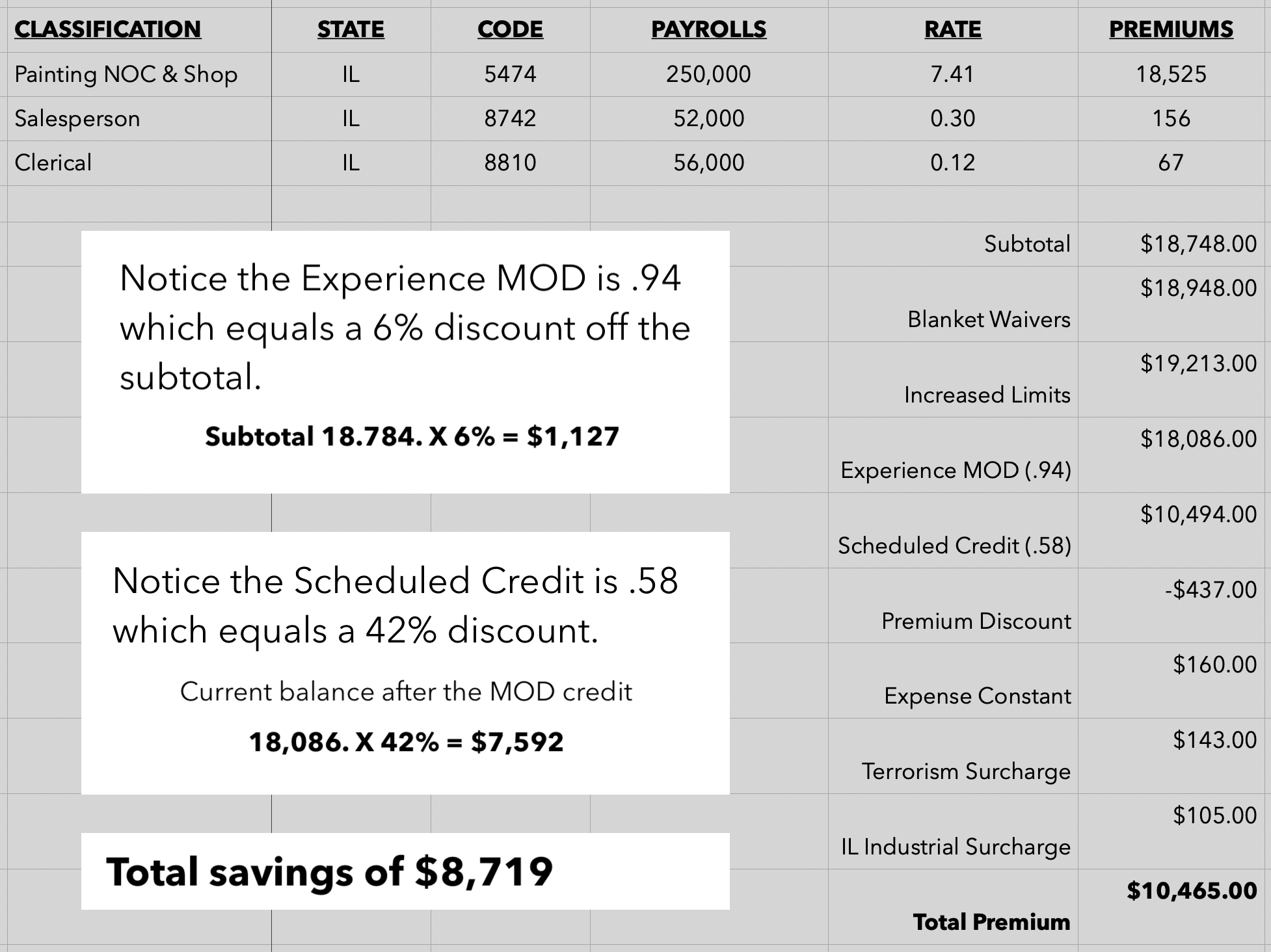

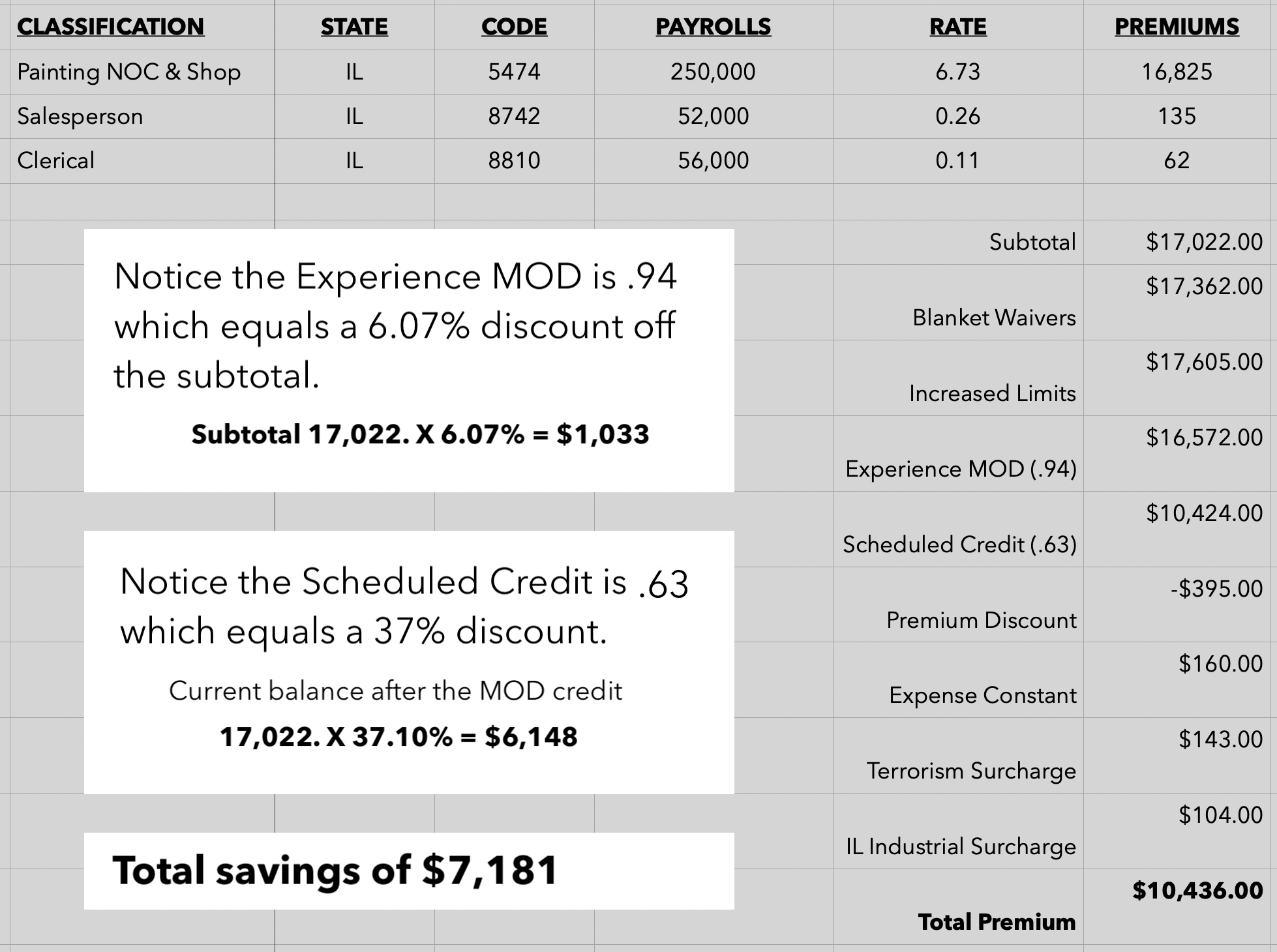

Year 1 vs Year 2: What Most Companies Miss

Experience Mod: 0.94 (6% discount)

Scheduled Credit: 0.58 (42% discount)

State Rate: 7.41

Experience Mod: 0.94 (same 6%)

Scheduled Credit: 0.63 (37% discount)

State Rate: 6.73

At first glance, the total premium appears nearly the same — making it easy to assume nothing changed.

In reality:

- The state rate dropped

- Your negotiated credit was reduced

- Your discount decreased

- Your net rate did not improve as it should have

If your prior scheduled credit had been maintained, your premium — and net rate — would have dropped significantly.

Why This Matters for BreakEven+™ and Forecasting

If your net rate is wrong or misunderstood:

- Your estimates are inaccurate

- Your break-even calculations are flawed

- Your forecasts become unreliable

- Your profitability appears misleading

Using FALIB®-Mr, FALIB®-Sr, and FALIB®-Jr, companies can connect estimating directly to real financial outcomes.

From Insurance Data to Financial Intelligence

The goal is not just to reduce insurance cost — it is to understand it, control it, and apply it correctly in your pricing model.

• Estimating becomes accurate

• Pricing reflects true cost

• Forecasting becomes reliable

• Financial reporting aligns with reality

This is the foundation of financial clarity — and exactly what FALIB® and BreakEven+™ are built to deliver.